Italian beauty industry grows and strengthens its global leadership

From Cosmetica Italia report: in 2025 turnover increased by 2.9%, driven by exports at +4.1%. Looking ahead to 2026, the industry is aiming for accelerated growth, supported by innovation, sustainability and evolving global consumption trends.

Despite the high level of uncertainty affecting the international geopolitical landscape, the Italian cosmetics industry closed 2025 with a total turnover of €18 billion, marking a 2.9% increase compared to the previous year and sending a clear signal of the competitive strength of Made in Italy worldwide. This is highlighted in the report “Outlook 2025 – Dynamics and perspectives of the Italian cosmetics industry” by Cosmetica Italia, the sector’s leading association.

From an operational standpoint, however, companies are facing increasing pressure on margins due to rising production costs and energy prices. These challenges are compounded by compliance requirements linked to new European ESG standards, with particular attention to ecodesign and packaging regulations (PPWR).

The domestic market

On the domestic front, sales reached €9.4 billion (+1.8%). Demand proved particularly resilient, with total consumer purchases amounting to €12.8 billion, up 3.2%. The e-commerce channel stood out, growing by 9.8% and confirming the ongoing digitalisation of consumption patterns. Among product categories, skincare leads the market with €4.3 billion (+3.2%), followed by haircare (€2.95 billion; +4.1%) and personal cleansing (€2.26 billion; +1.6%). Make-up remained stable at €1.72 billion, while fragrances, at €1.55 billion, recorded the strongest growth (+7.4%). Forecasts for 2026 confirm a strengthening consumer propensity to spend, with expected growth of 3.5%.

Exports: the United States leads, China surges

Once again, exports proved to be the main driver of the supply chain, accounting for 48% of total revenues and consolidating Italy’s position as the world’s fifth-largest exporter, with a 5.6% share of the global market, behind France, the United States, Germany and South Korea. Exports reached €8.6 billion, up 4.1%, making a decisive contribution to a strongly positive sector trade balance of €5.1 billion.

The United States remains the leading destination, with exports worth €1,174 million (+1.3% compared to 2024), followed by France (€873 million, -0.7%) and Germany (€783 million, +1.8%). Strong growth was recorded in Spain (+15.3%), Poland (+14.9%) and the Netherlands (+10.5%), highlighting dynamic consolidation across Europe.

In terms of categories, fragrances lead with €2,733 million (+6.4%), followed by skincare (€2,184 million, +2.3%) and haircare (€1,577 million, +3.0%). Make-up (€1,256 million, +1.8%) and personal cleansing (€824 million, +6.9%) also made a significant contribution to overall performance.

In Asia, the picture is more complex: the decline in exports to Hong Kong (-17.0%) and Taiwan (-27.2%) was more than offset by a sharp increase in China (+51.7%), confirming the country’s central role in Italy’s growth strategy. Sales are being driven both by the expansion of domestic e-commerce and the development of new duty-free hubs, such as Hainan Island, which is emerging as a key destination for luxury products.

Emerging trends in packaging

Consumer habits are being reshaped by the “multi-skinification” trend, where haircare and make-up products incorporate skincare claims and functionalities. At the same time, increasing attention is being paid to packaging designed for fast-paced lifestyles.

Focusing on inclusivity (e.g. accessibility) and outdoor use, packaging is evolving towards practical opening solutions alongside sustainability requirements, such as recycled and recyclable mono-materials. Innovation is moving between hyper-personalisation, a renewed focus on heritage ingredients reinterpreted in a modern way, and the enhancement of the sensory experience, in line with the trend of “revenge spending” on small luxuries.

Geopolitics takes a back seat to competition

According to industry players, factors such as US trade policy and the slowdown of the Chinese domestic market are perceived as marginal. Instead, the main concern is the expansion of Asian beauty brands, highlighting that the real challenge lies not in trade barriers but in direct competition from players capable of exporting highly innovative beauty routines worldwide.

Outlook 2026–2029

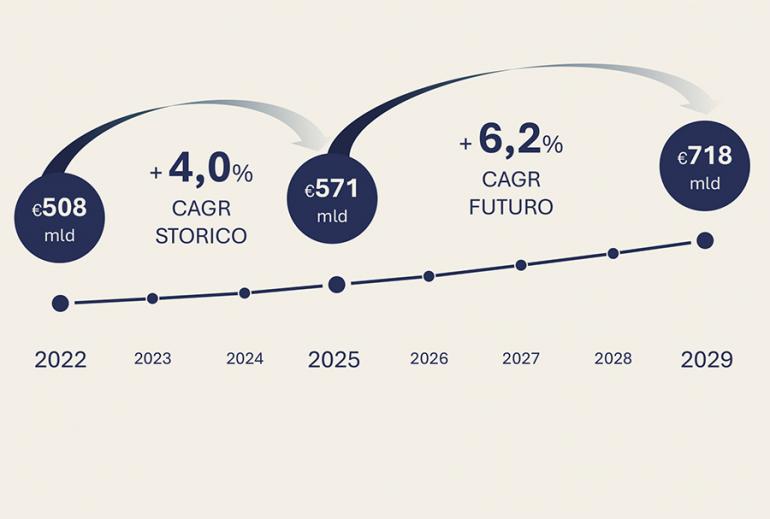

Forecasts for 2026 point to cautious optimism, with an acceleration in total turnover (+4%), supported by export growth (+5%). Looking further ahead, global beauty consumption is expected to grow above historical trends (+4%) and macroeconomic indicators, reaching an acceleration of +6.2%, although with significant differences across regions, categories and price segments.

Geographically, the main growth drivers will be Latin America (+8%), India (+7.6%) and the Middle East (+15% in pre-conflict estimates). Growth will be primarily driven by premium segments (+6.3%), while specialised channels such as perfumeries and pharmacies/drugstores will continue to play a key role in distribution.

Global beauty consumption is entering a phase of structural acceleration, driven by the boom of the fragrance economy and supported by the rise of new emerging hubs alongside China, including Brazil, India and the Middle East (despite uncertainties linked to ongoing conflicts). This is occurring within a context of increasing convergence between mass and premium segments: while price polarisation is currently evident, the gap between the two may narrow in the future.

This article appears in the Special: