Italy promotes online grocery

Italy is one of the countries showing a greater propensity to purchase grocery goods online. In 2023 the market recorded a jump of 7% against 2022, reaching a value exceeding 1.3 billion euros. The category showing the greatest growth is Pet Care (+25%).

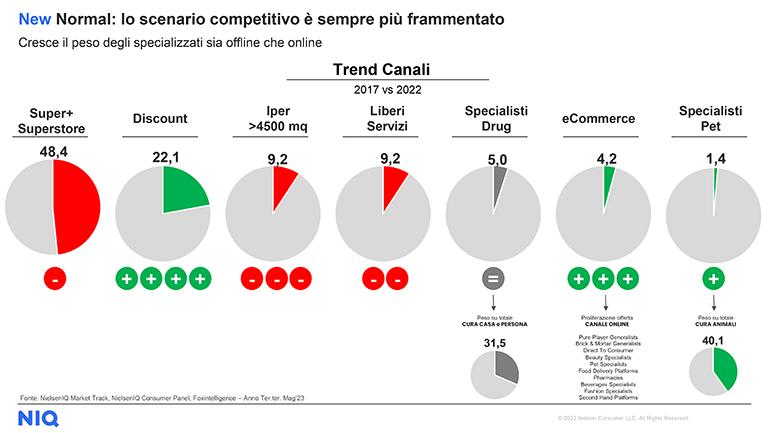

According to Netcomm Focus Food&Grocery*, the distribution of consumer goods scenario is confirmed as very fragmented, with omnichannel retail brands growing in the online channel by +10.7 against an average growth of +7%. Despite significant progress in recent years, particularly in the technologies field, e-commerce still has a marginal market share. We’re talking about 4%, in fact, with Super+ and Superstores together exceeding 48%, Discount stores at 22%, Hyper stores at 9,2% and Personal Home Specialists 5%. In absolute terms, Italians that today buy consumer products online in the territory number 10.8 million.

Widening the field, there’s an increase also at global level, but a slowdown in the trend: the global market share of grocery online has moved, in 2023, from 3.4% to 3.7% and is expected to arrive at 5.1% of the grocery market (online and offline) by 2025.

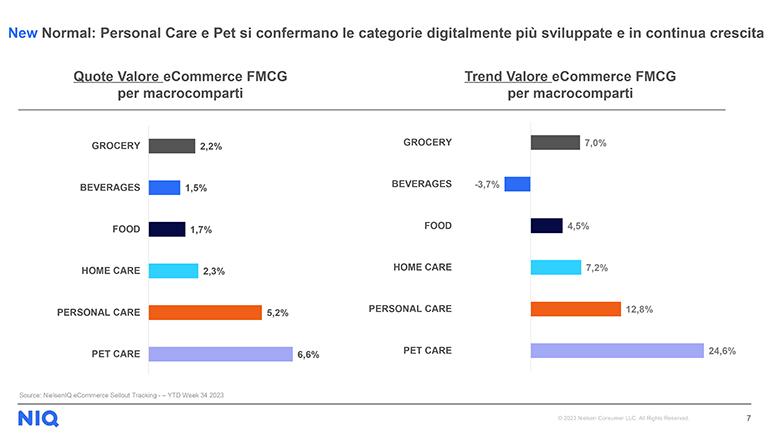

Coming back to Italy, two categories in particular were protagonists of growth in 2023: Pet Care and Personal Care, which recorded respectively +25% and +13% against 2022 and a share of total retail of 6.6% and 5.2%.

*The most recent research of Netcomm NetRetail, NielsenIQ and of the Food and Prices and Assortments Monitoring Centre in collaboration with Qberg were presented during the sixth edition of Netcomm Focus Food&Grocery (October 2023, Milan).

More than the price, it’s efficiency that counts.

Food expenditure is one of the categories with the greatest share with regards to purchases online. It is, however, a percentage which is down on the previous year (-12%) and is close to that that recorded in 2018, which was 23%.

It should be noted that Food is the only product category for which the price is not among the five main purchase drivers for digital consumers: the key factor is “convenience”, not understood as the lowering of costs but, instead, in terms of efficiency and, therefore, of time savings and the variety of services linked to delivery. Other important factors are inexpensive delivery, the assortment and habit. It’s interesting to note how the map of Food&Grocery purchases show an Italy at two speeds: while the area including Abruzzo, Molise, Puglia, Campania, Basilicata, Calabria and Sicily shows an increase of 24% compare to last year, in the more northern regions (Piedmont, Valle d’Aosta, Liguria and Lombardy) growth does not reach 3%.

Reciprocal influences. Is online in this sector able to condition consumers and push them towards offline sales? Not very much. With regards to spending for food/the home, in fact, purchasers in physical points of sale that have consulted at least one digital touchpoint before the purchase are a little over 15%. Online purchasers of the category that have arrived at the online choice through a visit to a point of sale are, instead, almost 40%.

Artificial Intelligence, a strategic ally. Netcomm Focus Food&Grocery provides us, finally, with a focus on artificial intelligence in the sector. The opportunities provided by AI, insiders confirm, will bring benefits to the entire food supply chain: from interpretation of customers’ needs to industrial processes, from logistics to the development of an effective marketing strategy. Today, artificial intelligence can intervene on interaction models with trolleys, with the possibility of creating “emotional” product selections conceived on the basis of the specific user and proposed as offers or suggestions at the check-out.